Coronavirus: the economic impact – 10 July 2020

10 July 2020 By the Policy, Research and Statistics Department, UNIDO. This brief is produced by a team consisting of Nicola Cantore (lead), Frank Hartwich, Alejandro Lavopa, Keno Haverkamp, Andrea Laplane, and Niki Rodousakis.

See a more recent brief on this issue: Coronavirus: the economic impact – 21 October 2020

By the Policy, Research and Statistics Department, UNIDO. This brief is produced by a team consisting of Nicola Cantore (lead), Frank Hartwich, Alejandro Lavopa, Keno Haverkamp, Andrea Laplane, and Niki Rodousakis.

Introduction

Widespread economic losses

The economic crisis unleashed by the outbreak of COVID-19 is hurting economies, regardless of income level. The most recent data from UNIDO’s seasonally adjusted Index of Industrial Production (April 2020 vs December 2019) indicate that both lower- and upper middle-income countries have been significantly impacted by COVID-19 (Table 1).

Table 1. Average loss in % in the Index of Industrial Production (IIP) across countries. April 2020 vs December 2019

Source: UNIDO elaboration based on our Statistic Data Portal.

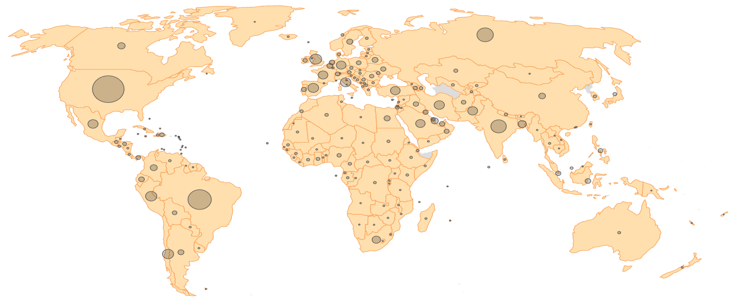

Economic losses are not correlated to health impacts

Recent data from the Centre for Systems Science and Engineering at Johns Hopkins University show that the spread of the pandemic in terms of case numbers and deaths is quite asymmetric across countries. Sub-Saharan Africa, for example, one of the poorest regions in the world, does not seem to have been severely impacted by COVID-19.

Figure 1. Spread of COVID-19 around the globe

Source: Centre for Systems Science at the Engineering at John Hopkins University

A study by Noy et al. (2020) finds that the direct costs of the COVID-19 pandemic associated with illness and mortality are lower than the indirect losses caused by the crisis. A low impact of COVID-19 in terms of case numbers and deaths does not necessarily translate into a low economic impact. [1] Many countries are experiencing a recession, even though COVID-19 has not had a serious effect on them in terms of health. Even minor public health events can severely affect firms in lower income countries due to their poor socio-economic conditions (vulnerability) and their weak capacity to respond to crises (resilience). Moreover, in a globalized world, many countries are suffering indirect consequences from value chain disruptions and lower international demand for goods due to widespread recession.

Section 1 presents recent evidence on the current state of industrial production and exports. Section 2 focusses on the impacts of COVID-19 on firms based on the most recent data collected by UNIDO in several Asian countries. Section 3 discusses the policy implications of our findings.

1. Industrial production and trade: the situation in April 2020

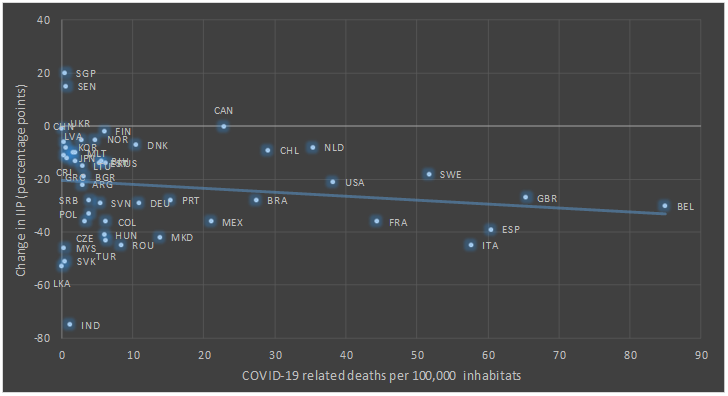

Huge economic losses are not necessarily associated with high health impacts

We use recent data derived from UNIDO’s Index of Industrial Production (IIP) for our analysis of 49 countries representing around 87 per cent of world manufacturing value added (MVA). A comparison of IIP data (adjusted to take seasonal effects into account) for March 2020 vs December 2019 shows that approximately 81 per cent of countries have experienced a decrease in industrial production of 6 per cent on average. A comparison of data for April 2020 vs December 2019 reveals that industrial production fell by 20 per cent on average in 93 per cent of countries. [2] As Figure 2 illustrates, a decrease in the IIP does not necessarily translate into a high impact in terms of health. Countries with a similar number of COVID-19-related deaths may experience different levels of economic loss, depending on the severity of the containment measures implemented or their indirect effects.

Figure 2. Relationship between decrease in industrial production and COVID-19 (April 2020 vs December 2019)

Note: Cumulative COVID-19 deaths per 100,000 population extracted from the Johns Hopkins University of Medicine.

Source: UNIDO elaboration based on our Statistic Data Portal.

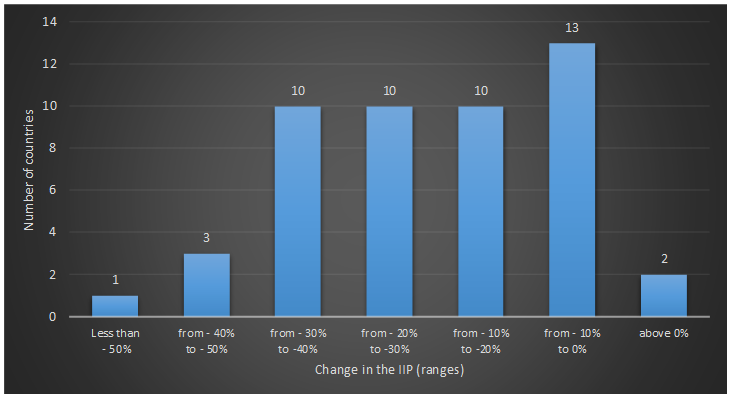

Heterogeneous impacts, but with negative signs

The distribution of decreases in industrial production is heterogeneous across countries and varies from positive values to losses of more than 50 per cent. India’s IIP fell by 65 per cent, reflecting the drastic cut in exports already flagged in a previous issue of UNIDO’s COVID-19 economic impact analysis. An interesting picture emerges when countries are categorized based on the decrease in their industrial production by comparing data from April 2020 and March 2019. About 50 per cent of the countries suffered a decrease in industrial production of over 20 per cent. The group of countries whose IIP fell between 20 per cent and 30 per cent represents the median of the sample. The group with decreases in IIP of between 10 per cent and 20 per cent includes the highest number of countries.

Figure 3. Distribution of decreases in IIP (April 2020 vs December 2019) across a sample of 49 countries

Source: UNIDO elaboration based on our Statistic Data Portal.

Industrial production across the globe deteriorated further in April 2020 compared to March 2020. It continued declining in 90 per cent of the countries included in our sample, with an average drop of 15 per cent within one month. Monthly reductions were further observed in India (- 55 per cent), North Macedonia (- 35 per cent), Malaysia (- 34 per cent), Turkey (- 33 per cent) and Slovakia (- 32 per cent). Countries that registered an increase in industrial production were Senegal (+ 9 per cent), Canada (+ 7 per cent) and Singapore (+ 4 per cent).

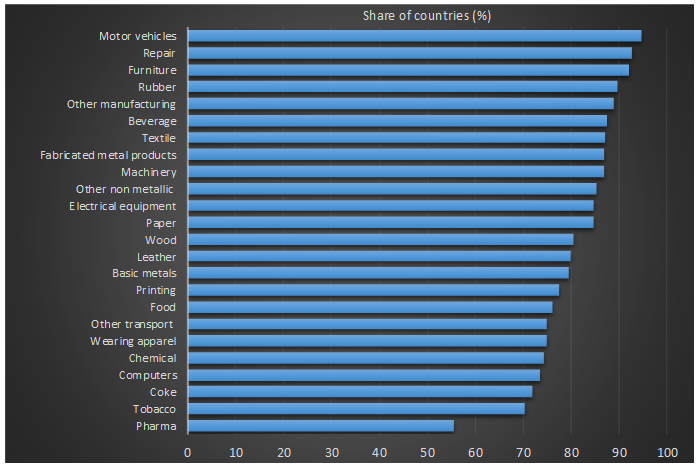

Manufacturing in crisis in many countries

All manufacturing industries were affected by the crisis over the period March 2019–April 2020. The share of countries that experienced a decrease in manufacturing varies from 55 per cent (pharma) to 94 per cent (motor vehicles). In a previous UNIDO COVID-19 economic impact analysis, pharma was actually identified as one of the very few “winners”, while motor vehicles was (and continues to be) one of the biggest “losers”. This demonstrates that the negative trend continued into April across all industries, even though some industries, such as pharma, seem to be slightly less affected than other more vulnerable industries.

Figure 4. Share of countries (%) registering a decrease in industrial production over the period March – April 2020 in different industries

Note: Industries according to indicator.

Source: UNIDO elaboration based on our Statistic Data Portal.

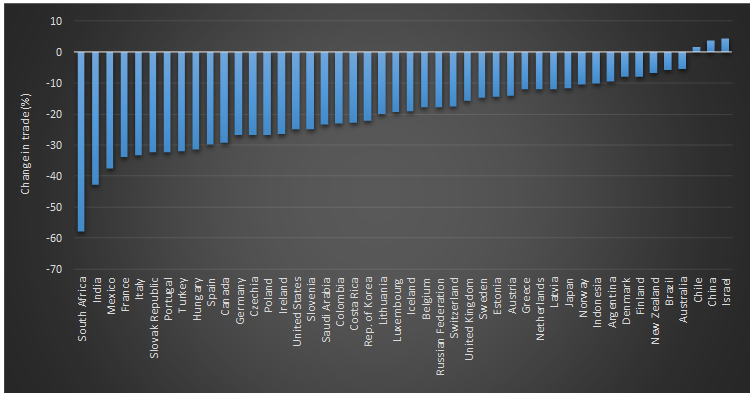

Trade losses for nearly all high- and lower income countries in March – April 2020

Over the period March – April 2020, trade trends closely followed those for industrial production. Forty-three out of 46 countries experienced a lower level of trade in goods. South Africa, India, Mexico, France and Italy are the five countries that suffered the highest reductions in trade volume over that period. Israel, China and Chile recorded an increase in trade. China further consolidated its path of rapid recovery, as already highlighted in a previous UNIDO COVID-19 economic impact analysis. Note that the top 10 countries with the highest reductions in trade volume includes both high-income and upper middle-income economies, reinforcing the finding in a previous issue of the UNIDO COVID-19 economic impact analysis that COVID-19 has a severe impact on both industrialized and developing countries.

Figure 5. Change of trade in goods in % by country for the period March – April 2020

Note: Countries according to indicator.

Source: OECD trade in goods statistics

These figures clearly show that the COVID-19 crisis has affected the majority of countries around the world. Fresh primary data collected by UNIDO in several Asian countries provides some preliminary evidence on the pandemic’s impact on firms.

2. A closer look at firms

Aggregate results ultimately hinge on what happens at the firm level

The economic impact of COVID-19 on the industrial sector ultimately depends on how the continued containment measures and related restrictions affect manufacturing firms. The extent of firms’ productive capacities, their degree of integration in domestic and global production networks and the type of market they serve are important factors determining the extent of the crisis’ impact on firms. Accordingly, some firms (and countries) are better suited to quickly respond and adapt their operations, thus reducing the shock’s overall impact on their profits, cash flow and staff.

However, firm-level evidence is still scarce

More than three months after the WHO declared COVID-19 a pandemic, harmonized firm-level industrial data remain limited, despite the avalanche of firm surveys initiated by national and international organizations. Aside from some country-level efforts to analyse the effects of the crisis on firms (most notably, the specific module on COVID-19 included in the 2020 ESIEC of Peking University), it is difficult to find manufacturing enterprise-level data that can be analysed and compared across different countries.

UNIDO is piloting firm-level surveys in several Asian economies

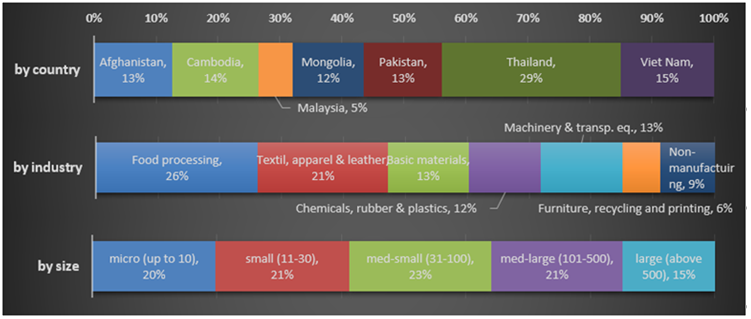

To fill this gap, UNIDO is piloting firm-level surveys across manufacturing firms in several emerging economies in Asia. The first round of the survey included seven countries and collected a total of 1,040 valid responses. It was implemented online between mid-April and early June in collaboration with governments, business chambers and other agencies operating in the participating countries. [3] The results obtained provide new insights into the differential impacts the crisis has had on countries, industries and types of firms, as well as into the main responses adopted by firms and governments. Figure 6 summarizes the structure of responses in terms of countries, industries and firm size.

Figure 6. Distribution of sample by country, industry and firm size

Note: Size is defined in terms of employees.

Source: UNIDO elaboration

The pandemic’s short-term impact differs widely across countries

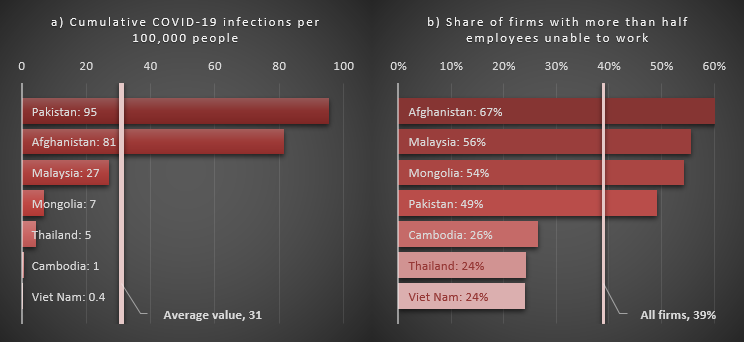

The impact of COVID-19 in terms of cumulative incidences in these countries per 100,000 population differed considerably across the countries surveyed (Figure 7, Panel a). While Pakistan and Afghanistan reported over 80 cases per 100,000 population, Thailand, Cambodia and Viet Nam had fewer than five cases. These differences are also partially reflected in the share of firms that stated that more than half of their employees were unable to work during the survey period (Panel b): firms in Afghanistan and Pakistan were affected more heavily than those in Thailand and Viet Nam. Over half of the employees of a very large share of firms in Malaysia and Mongolia were also unable to perform work, indicating that the actual number of COVID-19 infections was not the only factor at play. On average, more than one-third of the firms surveyed claimed that at least half of their workforce was unable to work.

Figure 7. The current impact of COVID-19 in selected Asian countries

Note: Countries according to indicator. Cumulative COVID-19 infections per 100,000 population extracted from the European Centre for Disease Prevention and Control.

Source: UNIDO elaboration.

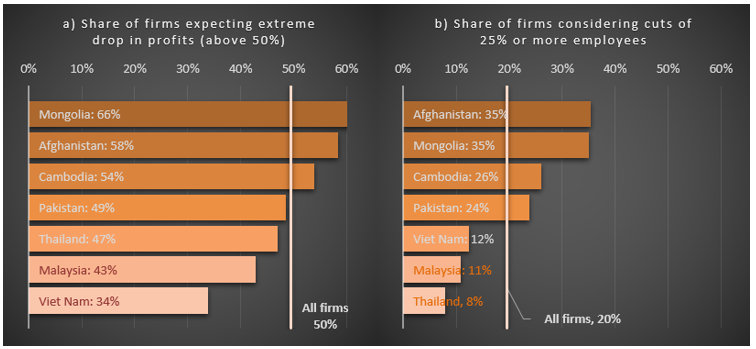

The prospects for profit and job growth are equally gloomy

The results on firms’ expectations about future profits and employment growth are less dispersed across countries, and portray a gloomy picture. Half of the firms surveyed expect a drastic decline in company profits (50 per cent or higher) for the year 2020 (Figure 8, Panel a). Moreover, 20 per cent of firms stated that they had to lay off employees or are planning to cut one quarter or more of their staff (Panel b). The largest share of firms expecting massive cuts both in terms of profits and employment is in Mongolia and Afghanistan.

Figure 8. The expected impact of COVID-19 on firms’ profits and employment, by country

Note: Countries according to indicator.

Source: UNIDO elaboration.

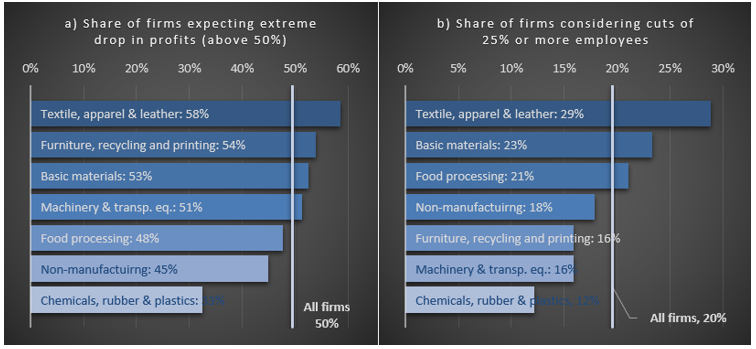

Not all industries are equally affected: textile and apparel firms expect to be the hardest hit; chemical and plastic expect to be the least impacted by COVID-19

Firms in the textile, apparel and leather industries tend to anticipate the largest plunge in profits and jobs, while firms in the chemical, plastic and rubber industries expect below average decreases (Figure 9). The basic materials industries also expect their profits and employment to be hit hard. In the furniture, recycling and printing industries, a large share of firms is anticipating a serious decline in profits (54 per cent), but only 16 per cent expect that they will be forced to announce drastic job cuts, which lies below the average share of firms included in the survey. Similar trends are observed in the machinery and transport equipment industries.

Figure 9. Expected impact of COVID-19 on firms’ profits and employment, by industry

Note: Industries according to indicator.

Source: UNIDO elaboration.

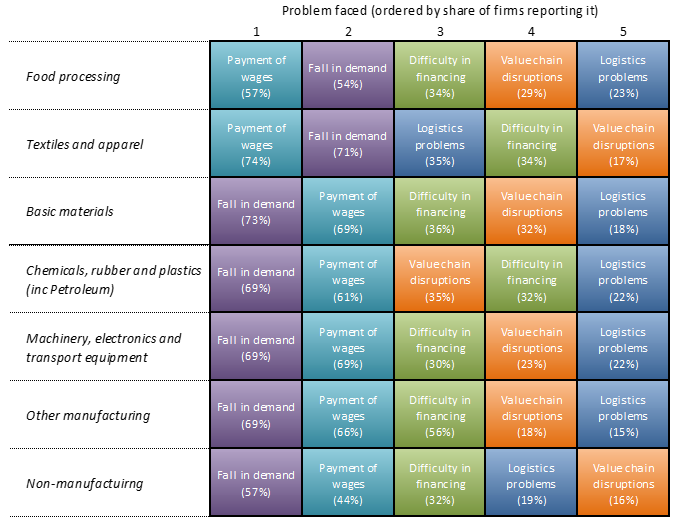

The main problems firms are facing also differ across industries

The different expectations across firms arise from the very challenges they face (Figure 10). Two major challenges widely reported by firms are 1) the contraction in demand, and 2) the payment of wages. The most pressing problem in labour-intensive industries (such as textile and apparel) seems to be the payment of wages. The plunge in demand is a widespread concern among other industries. Firms in the textile and apparel industry are also particularly concerned about logistics problems, while upstream and downstream chain disruptions are deemed a more serious problem for firms in the chemical, rubber and plastic industries than for other industries.

Figure 10. Top 5 problems reported by firms, across industries

Note: The values in brackets indicate the share of firms in the industry that reported this particular problem.

Source: UNIDO elaboration.

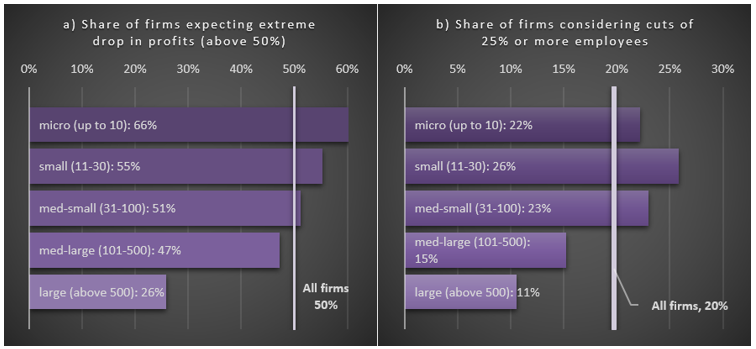

Differences also exist across firm size: SMEs are expecting a larger decrease in profits and more job cuts than large firms

Size also matters: smaller firms, on average, tend to anticipate a much larger decline in profits than larger firms (Figure 11). The same applies to job cuts, although micro firms are expecting to slash fewer jobs than small and medium-small firms.

Figure 11. Expected impact of COVID-19 on firms’ profits and employment, by firm size

Note: Bars according to firm size. Only manufacturing firms are considered.

Source: UNIDO elaboration.

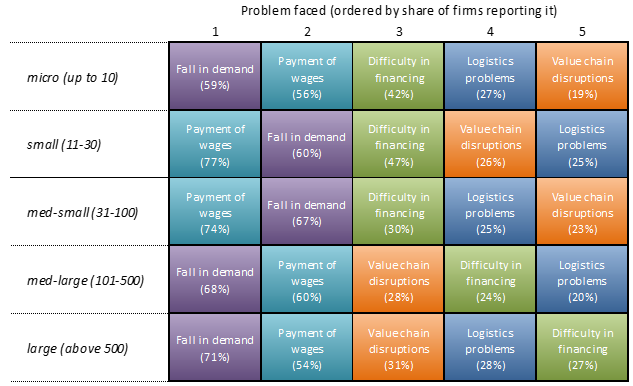

The problems small firms are dealing with are not necessarily the same as those larger firms are facing

The payment of wages seems to be more problematic for small and medium-small firms. By the same token, difficulties in financing are less relevant for medium-large and large firms. For them, value chain disruptions triggered by the COVID-19 crisis represent a far more pressing problem.

Figure 12. Top 5 problems reported by firms, across size

Note: The values in brackets represent the share of firms in the industry that reported this particular problem. Only manufacturing firms are considered.

Source: UNIDO elaboration

Firm heterogeneity calls for tailored policy responses

A general conclusion that can be drawn from these results is that not all firms are affected by COVID-19 the same way. Differences are observed across countries, industries and firm size. The type of problems industries and firms face also differ across different firm types. It follows that the policy responses implemented by governments to support firms in their recovery efforts should be tailored to account for these differences.

3. Policies and coping strategies

In this section, we provide further insights from the survey to examine the policies that have been implemented to date and their effectiveness. The findings must be viewed in the context of each country and region, but a rapidly changing trend for policy actions is visible, which has shifted from a focus on companies’ and households’ cash flow problems towards measures that support industries in adjusting to changing business conditions and that increase their resilience and help them develop systemic competitiveness in a newly structured global production network.

The type of support firms are receiving varies across countries, with tax deferrals being the most widespread measure

The most common forms of support reported by firms are tax deferrals or reductions, cuts in utility costs, deferment of loan obligations, concessional financing for firms that do not lay off workers and other types of financial assistance. The emphasis on deferrals of tax obligations seems to follow a global pattern. In their analysis of how OECD and G20 countries are responding to the COVID-19 crisis, Bulman and Koirala find that the deferment of taxes and social security payments is the most common fiscal instrument being implemented. Accordingly, as of 13 May 2020, 96 per cent of the 90+ countries covered by the OECD’s COVID-19 Policy Tracker had adopted such measures, followed by credit subsidies to firms (93 per cent), income support for households (91 per cent) and wage subsidies (89 per cent); cuts in taxes/social security and cash transfers/grants to firms were the least commonly used support measure (80 per cent and 51 per cent, respectively).

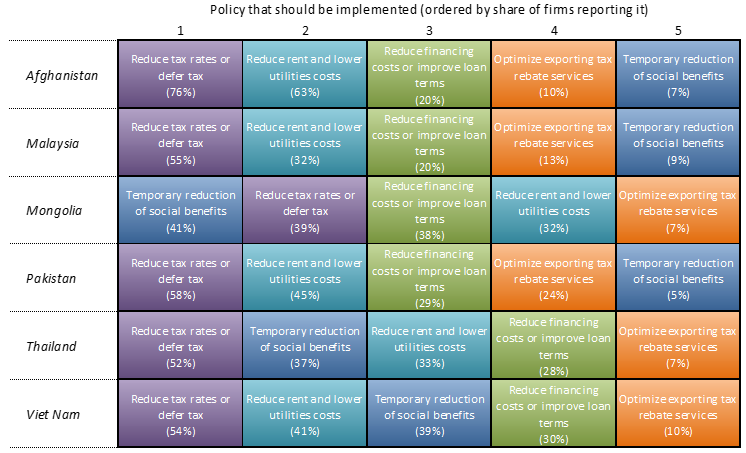

Firms are calling for tax cuts to respond to the crisis

The vast majority of respondents participating in the UNIDO firm survey stated that reductions in taxes and rent or in utility costs are measures they would applaud. The share of firms in favour of tax reductions ranged between 39 per cent (Mongolia) and 76 per cent (Afghanistan); the share of firms calling for reductions in rent and utility costs varied between 32 per cent (Mongolia) and 63 per cent (Afghanistan), as illustrated in Table 2. This result is consistent with the findings of the World Bank Survey monitoring COVID-19 impacts on firms in Ethiopia, with the peculiarity that the majority of Ethiopian firms consider tax payment waivers to be the most appropriate policy measure to help them cope with the challenges the pandemic has brought.

Table 2. Policies governments should implement, as indicated by firms (%)

Source: UNIDO

The effectiveness of fiscal measures

The UNIDO firm survey (covering Malaysia, Mongolia, Pakistan and Thailand) (see Section 2) also asked firms to indicate how useful the support measures provided by the government have been. Not surprisingly, direct financial support was considered the most beneficial support measure (72 per cent in Mongolia; 77 per cent in Pakistan; 73 per cent in Thailand). This sentiment is in line with a more general trend. The OECD recently analysed the expected impact of three types of government measures aimed at assisting businesses in coping with the financial fallout caused by COVID-19: (i) deferral of taxes; (ii) financial support for debt payment; and (iii) temporary support for wage payments. Two scenarios were considered in the analysis which relied on firm-level financial data from the Orbis dataset: one scenario in which government support for firms is abundant, and a second scenario in which no such support is in place. Supporting wage payments appeared to be considered particularly effective, while tax deferrals were found to have the least impact on firms’ cash flow. According to the same study, combining the three types of measures over two months would reduce the number of cash-strapped firms by 20 per cent.

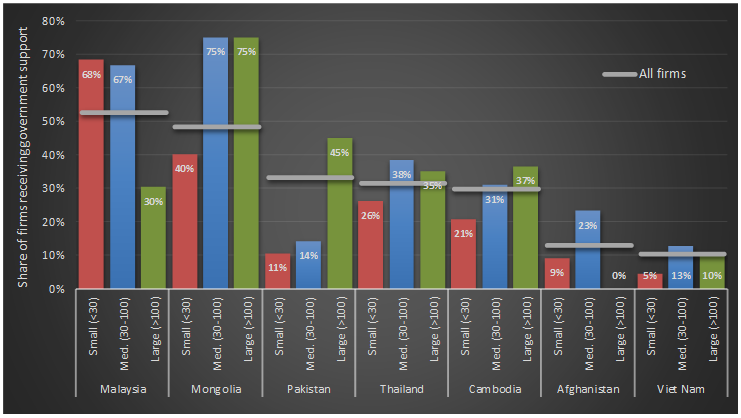

Larger manufacturing firms seem to be the primary beneficiaries of government support

The results of the UNIDO firm survey (see Section 2) also highlight the importance of government capacity for swift and effective responses to shocks. By capturing some of the characteristics of the support currently being provided to firms as opposed to firms’ expectations, we discuss options that could help governments design and adapt their industrial policy measures and packages.

We find that the average share of firms benefitting from government support measures or stimulus packages ranges from around 10 per cent (Afghanistan and Viet Nam) to 50 per cent (Malaysia and Mongolia). Overall, larger firms were more likely to receive support than smaller ones (Figure 13), which in “normal” times already tend to be more vulnerable and face more difficulties in accessing finance. A clear exception was observed in the case of Malaysia, where nearly 70 per cent of small firms surveyed received some form of support.

Figure 13. Share of firms benefitting from government support by firm size (%)

Note: The criteria for classifying firms by size varies across countries. Figures for medium-sized firms in Malaysia and Mongolia include medium-large firms.

Source: UNIDO

A shift towards conditionality

The impact of COVID-19 on businesses and the subsequent recession have prompted many governments to explore the option of making businesses more conducive to inclusive, sustainable growth. For example, the EU Recovery Plan for Europe envisages that the EU Recovery and Resilience Facility, together with the Just Transition Mechanism, will focus on investments in line with Europe green and digital transitions. The IMF is calling on countries to implement green recovery plans when elaborating the structural reforms necessary for further macroeconomic development. Individual countries are following a similar path: the Republic of Korea, Germany and the United States, for example, are promoting the greening of the construction sector (IISD 2020). Others are using state funds allocated for COVID-19 recovery to build more resilient healthcare systems (WHO 2020) or to reduce their dependence on imports of essential goods. This implies that the funds governments are allocating to mitigate the effects of the pandemic have become more conditional, and could eventually lead to a healthier, more resilient and productive economy (Mazzucato and Andreoni, 2020). For this to become a reality, however, governments must restore their capacity to design, implement and enforce conditionality among the recipients of financial support.

Some implications and some guidance: moving forward, developing countries need to start preparing for a resilient, inclusive and sustainable industrial recovery

Governments around the world and the international community at large have mobilized efforts to cushion the immediate effects of the crisis, especially in the developing world, with the countries covered in our analysis being no exception. However, the fact that SMEs are less likely to receive government support—in line with the fact that they generally face more obstacles in access to finance—serves as a warning sign and calls for improved policy responses to address the additional problems such firms are dealing with due to COVID-19. The composition and development of policy mixes throughout the different stages of the crisis as well as their effects on businesses and industries is another area that deserves attention. These effects should be continuously monitored as soon as the relevant data become available. In this regard, our analysis also sheds light on the absence of a visible strategy and policies to support business resumption and reorientation. How developing countries tailor these measures today will affect their prospects for building resilient, inclusive and sustainable post-crisis industrialization in the future. China, Europe and the United States have already initiated aggressive plans to reignite and bolster their productive capabilities and innovation. Developing countries must also seize the opportunity and start preparing now to prevent the existing asymmetries from widening even further.

[1] For example, according to a recent report of the African Development Bank, African countries—though many of them have so far not been significantly affected by COVID-19—are projected to contract by 1.7 per cent in 2020, dropping by 5.6 percentage points relative to the January 2020 pre-COVID-19 projection.

[2] A comparison between April 2020 and March 2019 as well as between March 2020 and March 2019 shows similar results (an increase in the average decrease in IIP and in the number of countries affected).

[3] The surveys were implemented with the support of the Regional Division of Asia and the Pacific and UNIDO field offices in the respective countries and were carried out in cooperation with the following partners: Afghanistan: Chamber of Commerce and Industries for Women; Chamber of Industries and Mines; Ministry of Industry and Commerce; Cambodia: Ministry of Economy and Finance, Ministry of Industry, Science, Technology and Innovation, The Cambodia Investment Board of the Council for the Development of Cambodia, Garments Manufacturers Association in Cambodia, European Chamber of Commerce in Cambodia, Cambodia’s Rice Federation, Young Entrepreneurs Association of Cambodia, Cambodia Women Entrepreneurs Association, UN Resident Coordinator’s Office, UN Economic Impact Group; Malaysia: Ministry of International Trade and Industry, United Nations Global Compact Malaysia Chapter and Federation of Malaysian Manufacturers; Mongolia: Ministry of Food, Agriculture and Light Industry; Mongolian Association of Leather Industry; Mongolian Wool Textile Association; National Association of Mongolian Agriculture Cooperatives; Mongolian Meat Association; Mongolian Food Industry Association; Pakistan: Ministry of Industries and Production; Small and Medium Enterprise Development Authority (SMEDA); PRGMEA; PFMA; PAPAAM; SIMAP; STAGL; Thailand: Ministry of Industry, Industrial Estate Authority of Thailand and Federation of Thai Industries; Viet Nam: Vietnam Industry Agency, Ministry of Industry and Trade and Agricultural Product Processing and Development Department, Ministry of Agriculture and Rural Development.

Disclaimer: This brief provides information about a situation that is rapidly evolving. As the circumstances and impacts of the COVID-19 pandemic are continuously changing, the interpretation of the information presented here may also have to be adjusted in terms of relevance, accuracy and completeness. The views expressed in this article are those of the authors based on their experience and on prior research and do not necessarily reflect the views of UNIDO (read more).

Original article: “Coronavirus: the economic impact", published on 28 March 2020.

First update: “The catchphrase may be uncertainty, but the losses are real", published on 20 April 2020 .

Second update: “Great uncertainty comes at a high cost and negative projections – but there’s some good news", published on 04 May 2020.

Third update: “Which countries and manufacturing sectors are most affected by the COVID-19 crisis? Some early evidence and possible policy responses", published on 26 May 2020.