COVID-19 impacts on industry: policy recommendations for the Arab region

By Massoud Hedeshi and Frank Hartwich

April 2020

This piece benefited from the support and contributions from UNIDO's Arab Regional Division and UNIDO Field Offices in the region.

Key Messages:

- The severity with which the COVID-19 crisis will hit Arab countries is determined by the degree of political stability and resilience inherent in the structure of their economies.

- Service-oriented, oil export-dependent economies are particularly vulnerable to COVID-19.

- A predominantly young population faces the risk of pronounced unemployment, but may also constitute a potential resource for effective national mobilization in recovery.

- Regional structural weaknesses can be turned into recovery opportunities for cooperation in sectors such as hospital equipment, manufacturing inputs, infrastructure, agriculture, fisheries and water supply.

Recommended policy options:

- Immediate: ‘Targeted’ and ‘blanket’ fiscal/financial support for all citizens and business entities,

- Medium term: Alleviation of structural imbalances through economic diversification,

- Continuous: Mass mobilization of youth in the sectors identified above.

Summary:

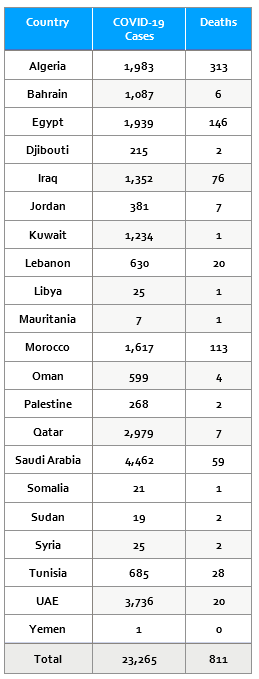

The Novel Coronavirus crisis has shocked and impacted the world in an unprecedented fashion, confining people to their homes while halting or otherwise negatively affecting most global production and trade for an unknown period. As a consequence, and further exacerbated by a poorly timed oil glut in the market caused by a 3-way price war’ between the largest global oil producers, global demand for fuel and energy has plummeted, slashing crude oil prices by 70 per cent in the first quarter of 2020. At the same time, tourism has virtually collapsed, and other industries face decreasing demand and supply. The combination of these interrelated dynamics has hit the Arab region particularly hard (though unevenly), despite COVID-19’s relatively low prevalence there as of 12 April 2020 (see Table 1). This paper discusses the specific characteristics of the crisis in the Arab region and their resultant policy implications and recommendations to enhance the region’s resilience to such shocks, and reinitiate the development of industries.

COVID-19 impacts in the region

In comparison with other regions, the total recorded COVID-19 cases and deaths in the Arab region remain relatively low, though their numbers are increasing (see Table 1). Nevertheless, all countries have already enacted or are about to enact some form of social distancing, curfew or lockdown. North African Arab nations appear to be most severely affected, followed by Iraq, Qatar and Saudi Arabia, while the situation in war-affected countries like Yemen, Syria and Libya remains unclear.

The crisis will place an additional substantial burden on the capacity of the public sector, particularly the healthcare system, while at the same time spreading infection rates may reduce medical staff and the availability of healthcare. For countries such as Algeria and Saudi Arabia, the pandemic is a double whammy: it has cut their major source of income at a time when social safety net costs are rising exponentially.

The impact on SMEs and their employees follows the global pattern: immediate closure of non-essential production, widespread loss of jobs and income, loss of remittances, repatriation of migrant workers and lower trade across borders. Informal sector workers and vulnerable groups with little savings, and the tourism industry as well as virtually all other non-medical exports of goods and services are bearing the brunt of the pandemic’s negative impact.

The region’s high unemployment and under-employment rates among youth will intensify during the COVID-19 crisis, particularly for daily labourers, underpaid (women) workers with irregular/informal contracts and migrant workers. On the other side of the coin, however, a younger population may prove more resistant to the adverse health effects of the pandemic.

Food security and safety are likely to become a significant concern if the current global situation continues, particularly in the region’s net food-importing countries. This could lead to urban-rural ‘reverse’ migration, coupled with rising costs of food staples.

War-torn countries in the region may benefit from a deviation away from war of those who fund, train and supply fighters, allowing them to refocus their efforts on fighting the pandemic. Overall, we should see a significant fall in arms trade and warfare across the region with a concomitant potential peace dividend.

At the same time, there will be a fall in demand for national currencies in lower-income countries and greater demand for real estate, gold and other precious metals as well as hard currencies. Some countries could also see bartering as an option for keeping up foreign trade as hard currencies may be in short supply.

Oil-dependence and regional characteristics at play

Inequality and uneven development are the hallmarks of the Arab region as a whole. As global stock markets continue to crash at a time when demand for oil is at the lowest it has been in decades, longer term prospects for oil exporters appear uncertain. Despite a recent OPEC++ agreement in principle to cut oil output by 10-15 million barrels per day, oil prices may continue to slide as global demand continues to fall even further.

Oil export-dependent and relatively rich countries with enormous financial resources and a highly educated citizenry have a relatively small population, and have struggled to diversify their economies as they lack the capacity to produce goods for local consumption and are highly dependent on foreign labour and expertise and the import of basic goods. However, these countries have the financial assets coupled with skilled manpower that together represent a significant resource for economic restructuring and much needed regional investment efforts, particularly in low-income and war-torn states.

While oil-importing, lower-income countries in the region may also have well educated populations, they have large numbers of underemployed and an overwhelming majority of young workers, lack financial resources, infrastructure, investments and employment opportunities, and, in some cases, suffer from political instability. For countries such as the Republic of the Sudan, Yemen and the State of Palestine, the loss of remittances from their migrant workers in the Persian Gulf countries and elsewhere constitutes a significant and immediate adverse effect. However, for these countries, as with most others globally, the availability of cheaper oil coupled with lower internal demand for heavily-subsidized fuel during an extended period of social distancing and immobility may, in fact, represent a windfall that may help widen the social safety net at a crucial time.

For labour-exporting economies potentially faced with a mass return of their skilled/semi-skilled migrant workers, the current oil glut presents an opportunity for stockpiling their energy reserves and redirecting scarce resources towards productive investments with low labour costs. This could result in reconstruction, employment generation and a reduction of imports of basic and intermediate goods, thus enhancing the countries’ economic diversification and resilience.

Countries such as Lebanon, Syria, Morocco and Egypt, which have developed basic to intermediate local agriculture and manufacturing capacity, are more diversified and amenable to structural transformation, and are expected to weather the COVID-19-crisis challenges better in the longer run. Furthermore, the existence of a large pool of underemployed and young population presents an opportunity for low-cost national mobilization in the face of adversity.

All categories of countries described above share the characteristics of poor access to arable land and drinking water, varying degrees of food insecurity and dependence on tourism and services, and are heavily impacted by the pandemic due to shortages in local medical goods and services as well as essential basic goods. Furthermore, they are losing industrial jobs at an alarming rate while their industrial output is drastically shrinking. Finally, a number of countries are affected by protracted, endless wars to varying degrees, be it in humanitarian, security, psychological or financial terms.

Economic response strategies

The current COVID-19 crisis has been caused by a sudden, virus-imposed collapse in the supply of labour in production and trade, coupled with the confinement of consumers, leading to a breakdown in demand for several goods and services. The nature of the current crisis therefore differs considerably to the 2007/8 financial crisis, and is widely expected to have a more profound and longer lasting negative impact globally.

Most economic response strategies (see IMF policy tracker) initiated in March have been fairly uniform, aiming at maintaining market demand through government-backed cash and credit support for households and SMEs, lowering the costs of utilities and regulating the price of basic necessities, with special attention to safeguarding the operations of banks. However, largely in line with the response strategy prescribed by the IMF during the 2008 ‘global financial crisis’, these recovery measures are likely to take months to translate into actions, particularly as they are prescribed as being ‘targeted’, which would necessitate ‘means testing’ at a time when public service offices and staff has been reduced or are otherwise compromised by lockdowns, illness and social distancing measures. They are also discretionary in nature, leaving much decision-making power in the hands of banks.

While essential, short-term liquidity in the market alone cannot be expected to help industries escape the crisis, and they will certainly not help diversify the region’s economies to make them more resilient to shocks from disruptions in global value chains. Additional measures to support manufacturers, especially SMEs, are needed for that purpose. Interesting cases have unfolded, for example, in Lebanon and Bahrain, where the measures that have been introduced are concrete, immediate and non-targeted, directly benefitting SMEs and recipient households and without overbearing means testing or targeting.

Disclaimer: The views expressed in this article are those of the authors based on their experience and on prior research and do not necessarily reflect the views of UNIDO (read more).